12.6 Backcasting

Sometimes it is useful to “backcast” a time series — that is, forecast in reverse time. Although there are no in-built R functions to do this, it is very easy to implement. The following functions reverse a ts object and a forecast object.

# Function to reverse time

reverse_ts <- function(y)

{

ts(rev(y), start=tsp(y)[1L], frequency=frequency(y))

}

# Function to reverse a forecast

reverse_forecast <- function(object)

{

h <- length(object$mean)

f <- frequency(object$mean)

object$x <- reverse_ts(object$x)

object$mean <- ts(rev(object$mean),

end=tsp(object$x)[1L]-1/f, frequency=f)

object$lower <- object$lower[h:1L,]

object$upper <- object$upper[h:1L,]

return(object)

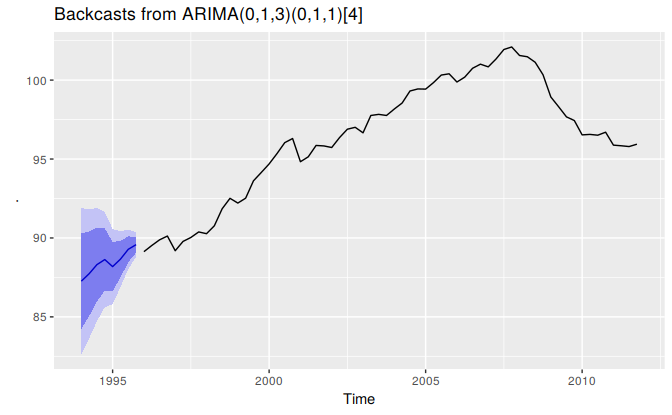

}Then we can apply these function to backcast any time series. Here is an example applied to quarterly retail trade in the Euro area. The data are from 1996-2011. We backcast to predict the years 1994-1995.

# Backcast example

euretail %>%

reverse_ts() %>%

auto.arima() %>%

forecast() %>%

reverse_forecast() -> bc

autoplot(bc) + ggtitle(paste("Backcasts from",bc$method))